Introduction

With the relaunch of Terra 2.0 on 28 May 2022, and the removal UST as one of its key USP, how should the new Terra perform in terms of valuations? Will it head to zero? Probably not, but is it still worth investing in? Let’s take a look.

What makes Terra interesting now as an investment is the UIUX, remaining community and developer base, as well as the potential for a new stablecoin and the amount of $CVX that they hold. Let’s explore each of them and how it is holding up against other Layer 1 protocols.

If you are wondering about the Luna airdrop distributions, details can be found here.

Revised Tokenomics

First off let’s take a look at the new tokenomics. Terra’s $LUNA can no longer be burnt to mint their stablecoin $UST, and now functions mainly as a staking token and governance token.

In terms of supply, it launched with a total supply of 1 billion, with 21% (210 million) currently in circulation. This is mainly given as an airdrop on day one to affected users. However, users holding wLuna, including Coinbase have not received the airdrop yet, so there is still impending sell pressure when this group of users receives their airdrop. As of writing this article, there is no news on when this airdrop will happen.

On top of that, the initial airdropped wallets below 10000 LUNA will start to linearly vest their LUNA from 25 November 2022 onwards for the next 1.5 years.

Additionally, developers will also be receiving an emergency allocation of 0.5% of the total $LUNA supply which will be sold at least partially to fund the development runway. Details can be found here. An additional 1.5% will be given out to developers at a later date.

Airdrop Distribution

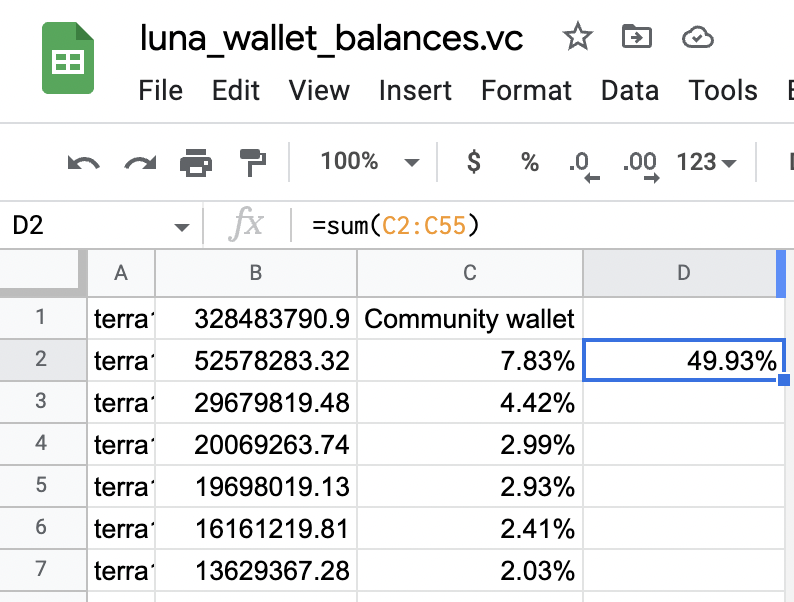

If we take a look at the wallet distribution, we will see that the top 54 wallets, excluding the community wallet of over 300m $LUNA, account for roughly 50% of all $LUNA distributed.

This distribution is heavily skewed toward whales and whale dumping risk is definitely high although most of the whales have their airdrop cliffed for one year (25 May 2023) if they had above 10,000 LUNA pre-depeg.

However, whales that bought LUNA and UST post-depeg still received 30% on genesis and there are various wallets with close to a million free-floating LUNA each ready to be ‘decentralized’ (read: dump) on exchanges.

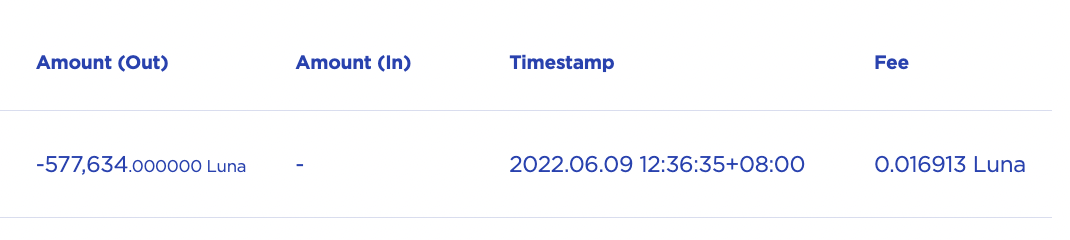

Checking through the top 100 wallets individually, most of the whale wallets did not send their luna to exchanges and are just sitting idle.

Less than 5 sold near the first day.

There were a few wallets that sent their $LUNA out, however, it is unclear whether it is being sent to an exchange or not as the wallets are unmarked. The recent negative price action could perhaps be a result of many retail offloading their unvested $LUNA or others that bought earlier on and are cutting their losses, and a small group of whales selling their airdrop bags.

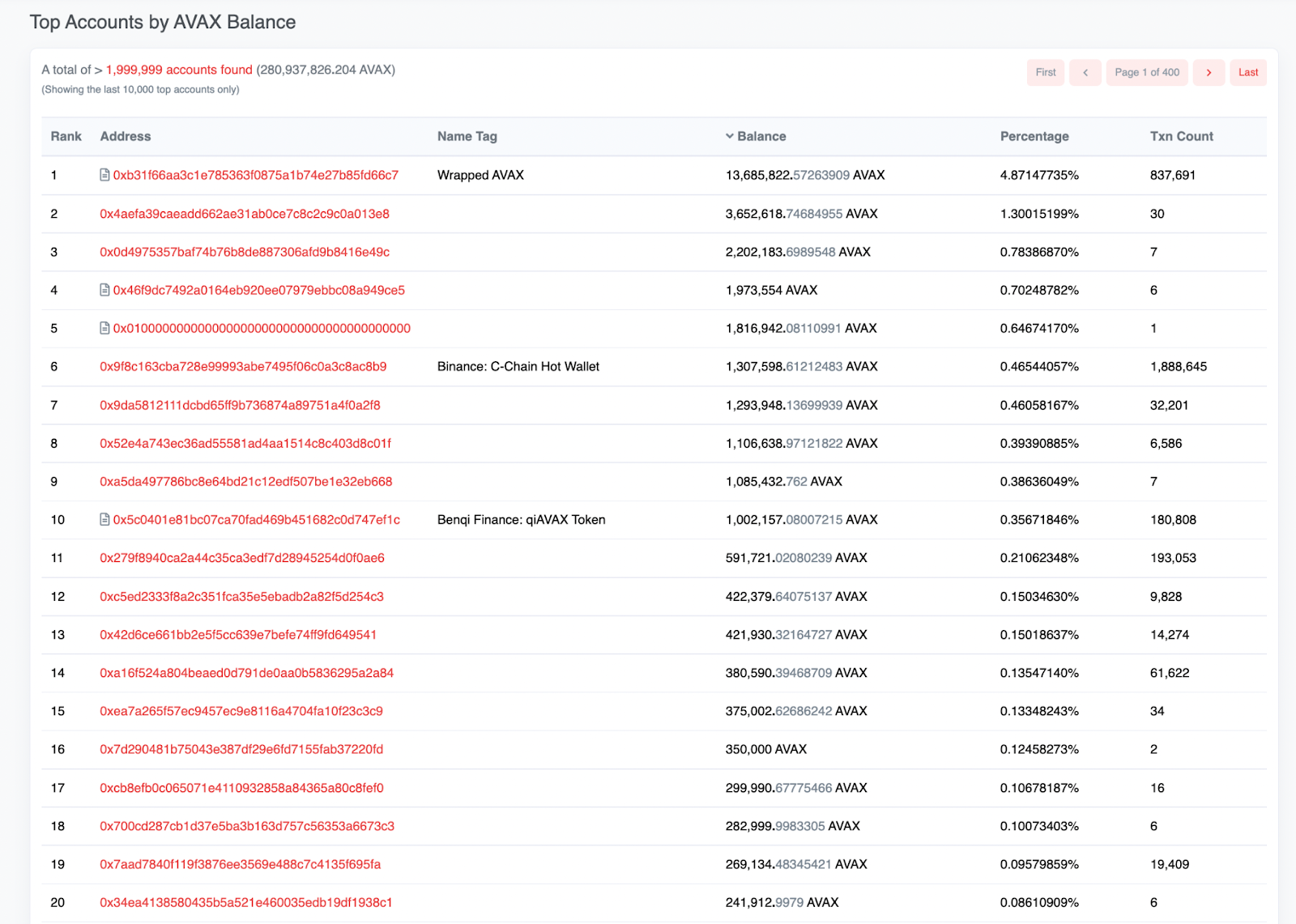

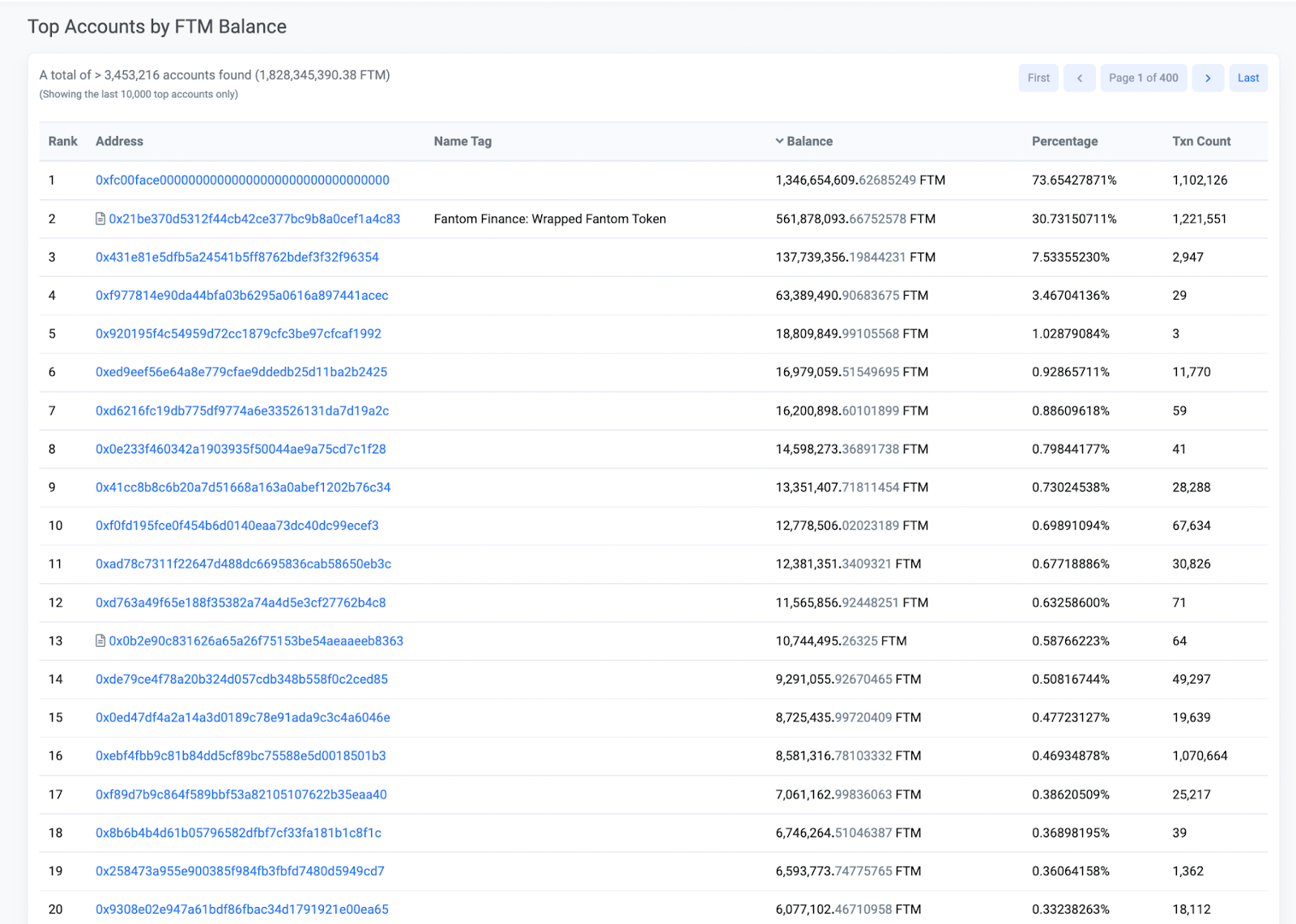

Compared with other EVM chains like avax and fantom, most of them are currently better distributed than LUNA. I am unable to find the wallet distributions for other chains at the moment. It is expected that over time the distribution will improve as whales decentralize their LUNA onto the market.

Staking Rewards & Emissions

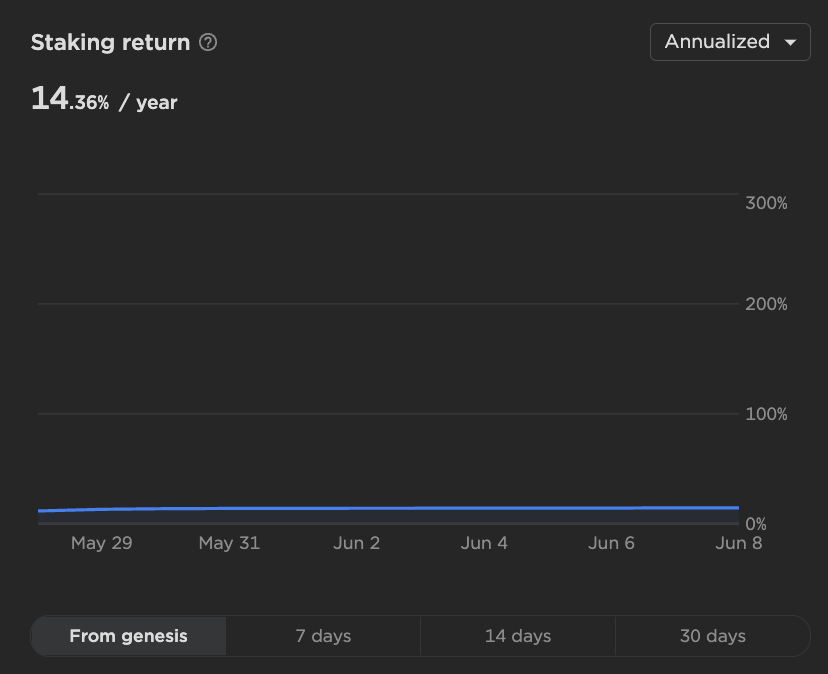

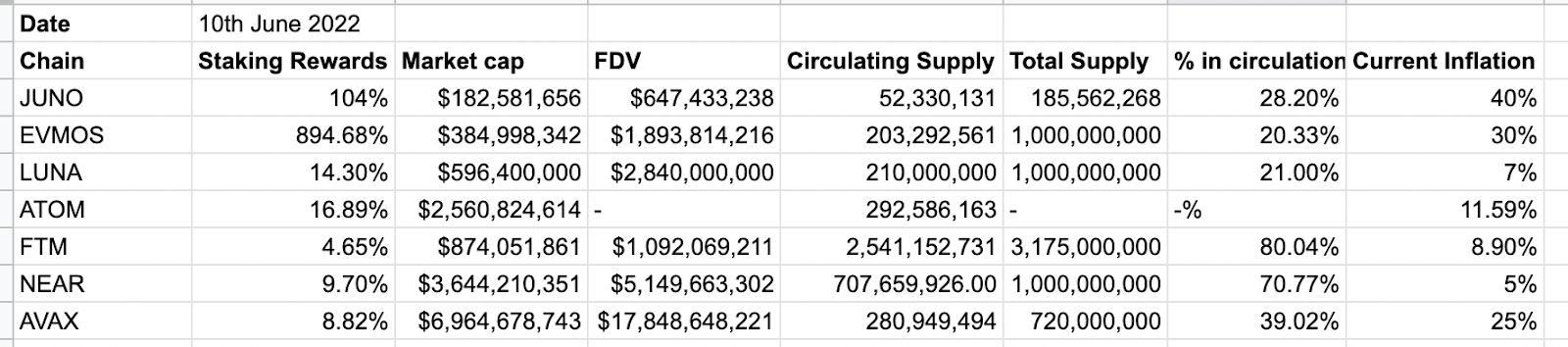

Currently LUNA’s staking returns, aka staking rewards, is projected to be around 14% a year, in LUNA tokens. Let’s explore other chains and see how it holds up.

Staking rewards for LUNA used to come from the LUNA and UST swap fees as well as gas fees, but the swap fees were the main driver.

With that revenue being gone, now the staking rewards come from annual inflation of 7% (unless changed) as well as from gas fees. This means the starting total supply of 1 billion increases by 7% a year until a burning function is implemented.

There is no max supply. Until it implements a burn function, LUNA is currently an inflationary infinite mint asset, a far cry from how it used to be referred as a deflationary apex asset.

The staking return is currently projected to be around 14% a year, which is comparable with other layer 1 chains but the lowest in terms of a cosmos chain. Below is the staking rewards of $LUNA compared with a few other similar chains from EVM and Cosmos.

Luna’s circulating supply of 21% means there’s still a large amount of $LUNA emissions left to go as well compared to other EVM chains.

All in all, the combination of no burning, infinite supply, whale wallets, and more incoming airdrops means investor beware, there is a lot of future selling pressure to go.

UIUX

The new Terra network still uses the same Terra Station which has a great UIUX. Sending $LUNA and performing transactions on the chain is still cheap, costing less than 10 cents for most transactions, and each transaction goes through in seconds, usually without any hiccups. Overall the experience is still great.

Speaking of chain running smoothly, during the fallout of Terra 1.0, the network did not go into a complete shut down even with the increased network activity and some validators dropping off. It was however congested for minutes at a time, but operated smoothly during the entire collapse.

This is fairly impressive considering how often other layer 1s get congested which leads to slow and high gas transactions almost daily during the bull market. This is a testament to cosmos chains being able to handle thousands of transactions per second with low block time of 2-6 seconds.

Overall, Terra’s UIUX continues to be smooth and was what made me a believer in the ecosystem, but UIUX alone is not enough. Polkadot with its unpolished UIUX has performed much better in terms of valuations due to strong backing and steady development, which brings us to our next point.

Community

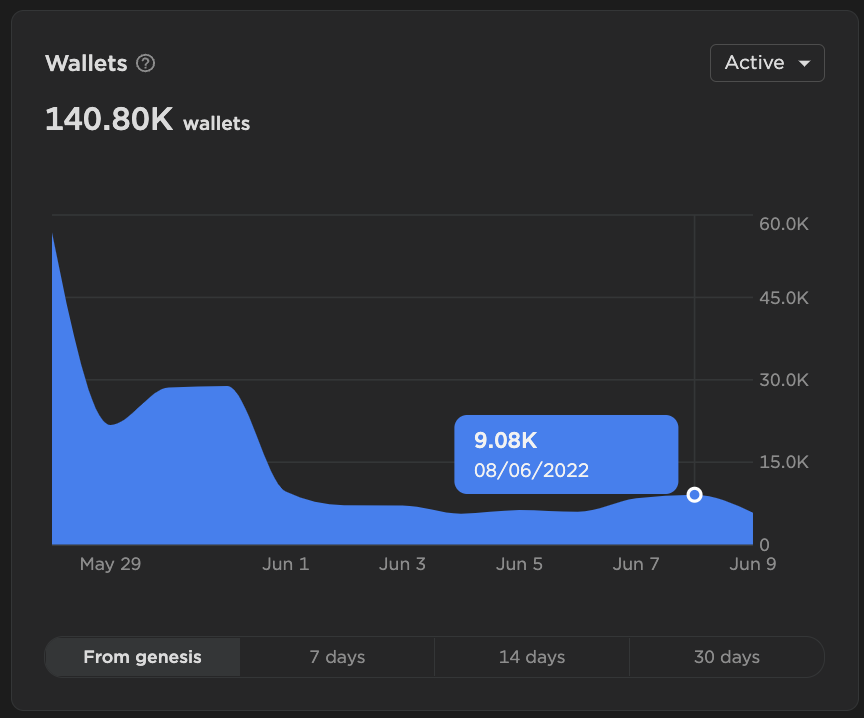

Based on Metcalfe’s law, the growth in active wallets typically corresponds to the growth in ecosystem value. Let’s explore the growth in Terra’s wallets.

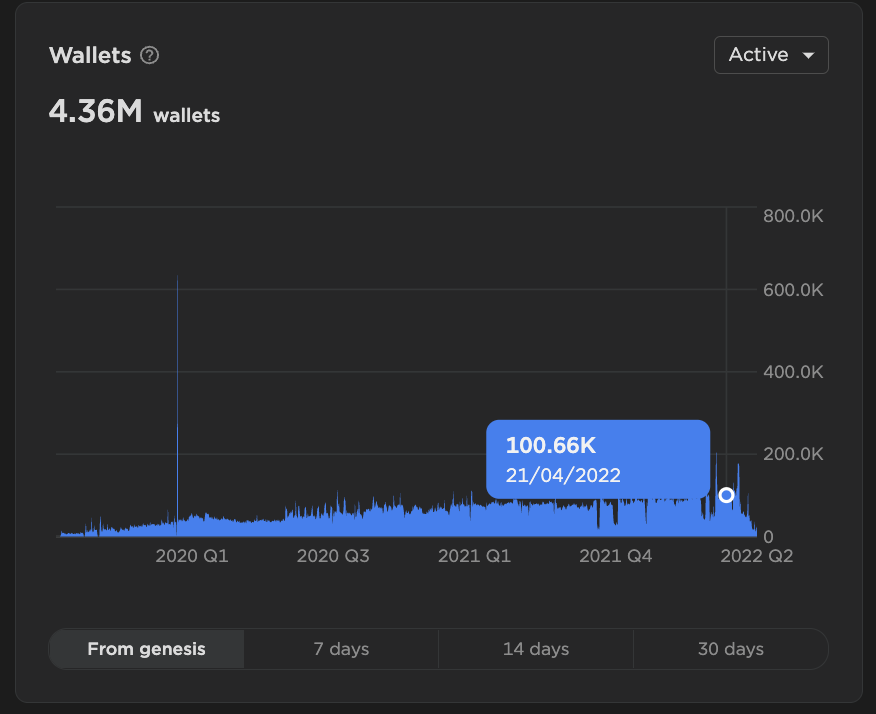

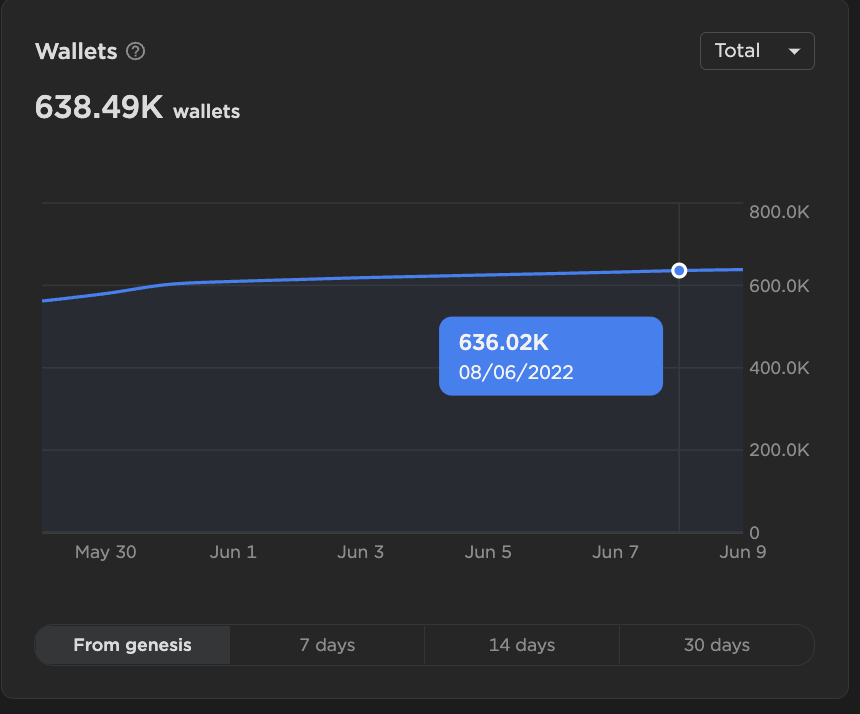

First off we’ve seen a huge drop in the number of active wallets between the original Luna and Luna 2.0, with an average of 100k active wallets in the original Luna to less than 10k in active wallets in Luna 2.0.

Granted that this huge drop is probably because there just simply isn’t much to do on Luna 2.0 at the moment and the trust has been lost. I expect to see this number trend upwards if developers start to build interesting protocols on it.

Luna 2.0:

Luna Classic:

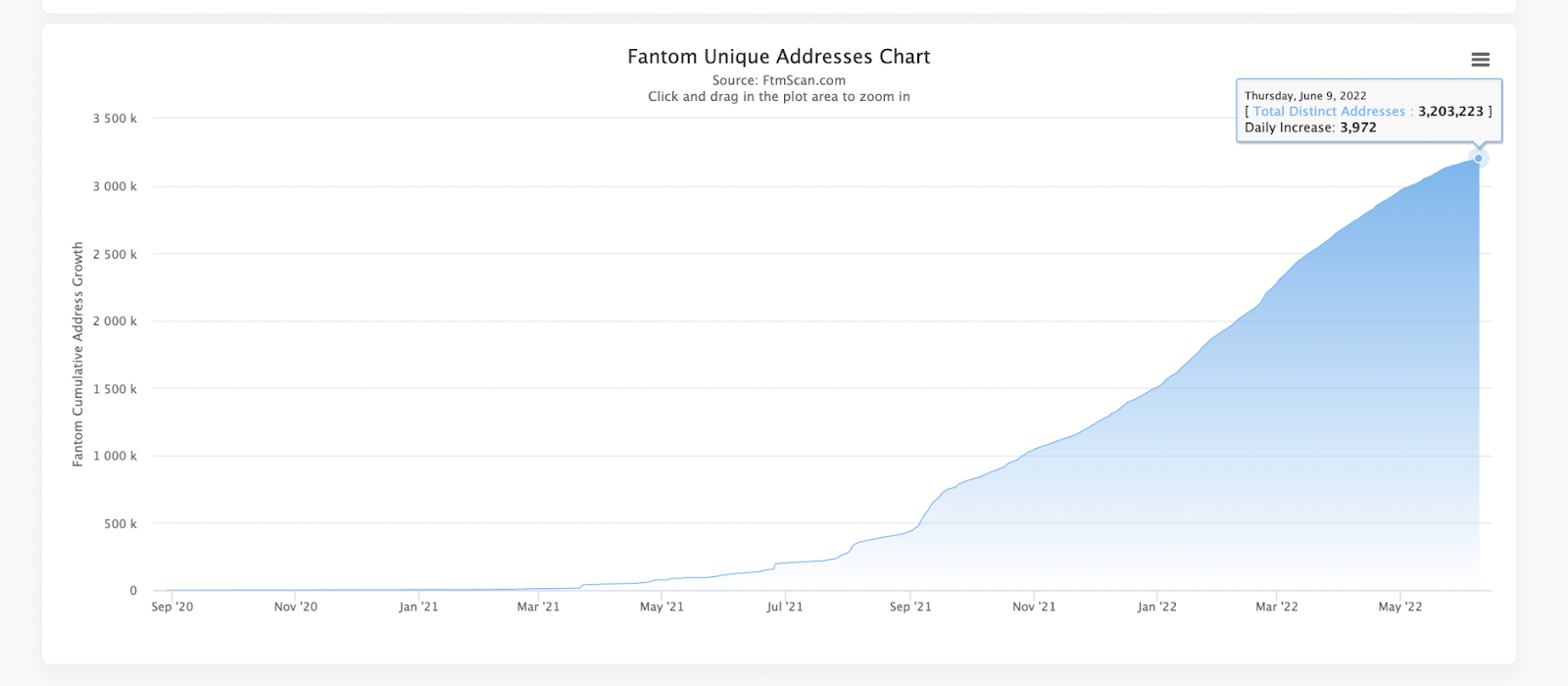

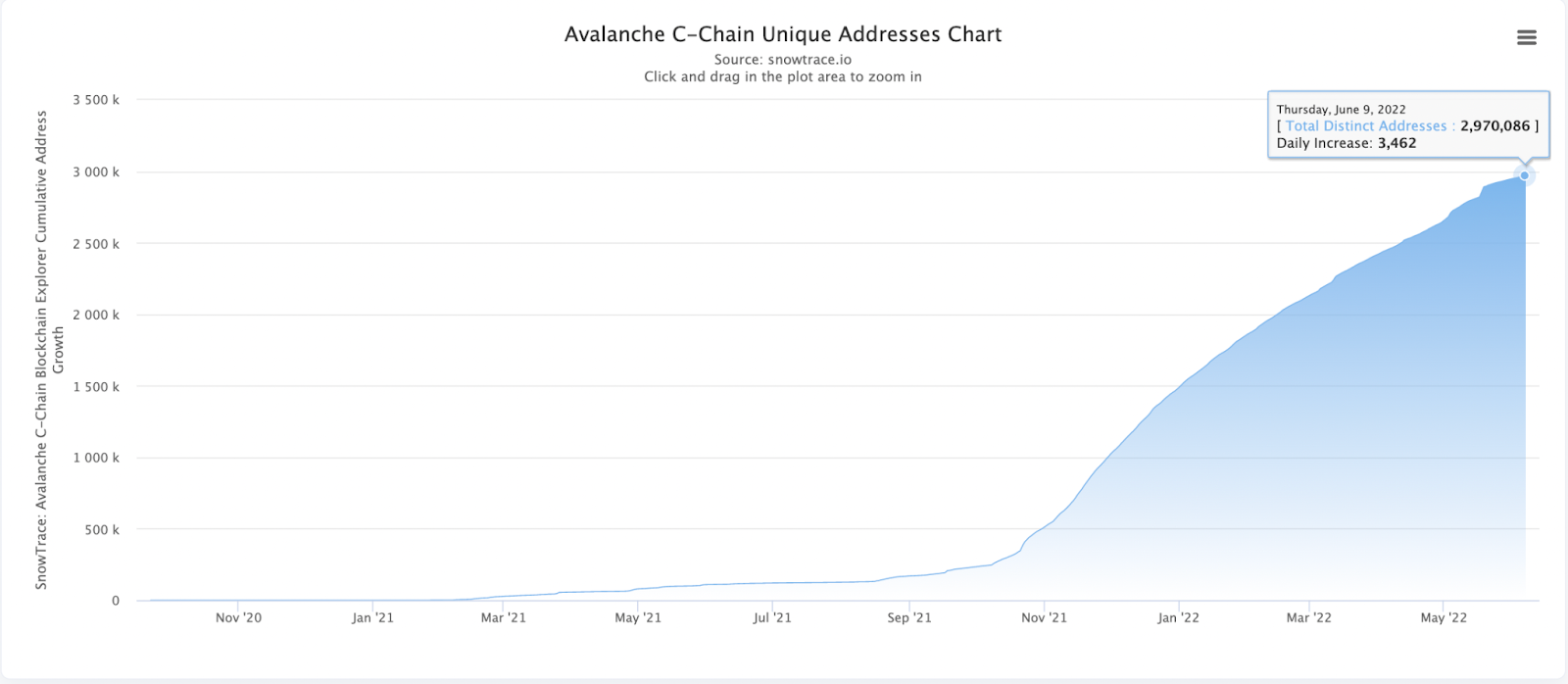

Looking at daily user growth, we see an average of about 2k to 5k new wallets on a daily basis since the launch. This is comparable with Fantom and Avalanche with around 3k-4k new wallets created daily as well. In terms of total wallets, Terra 2.0 has about 638k wallets right now, compared to 3.2m in Fantom and around 3m in Avalanche.

Developer Base

With many DApps being decimated during the collapse, a lot of DApps were initially not going to be part of Terra’s relaunch, however, some of them eventually decided to lauch back.

Here’s a look at Terra 2.0’s ecosystem. Apart from Astroport and a few others like Stader, Eris, and Phoenix, most of the dapps are still in development for Terra 2.0.

Credit: https://twitter.com/Speicherx/status/1534252509266853888

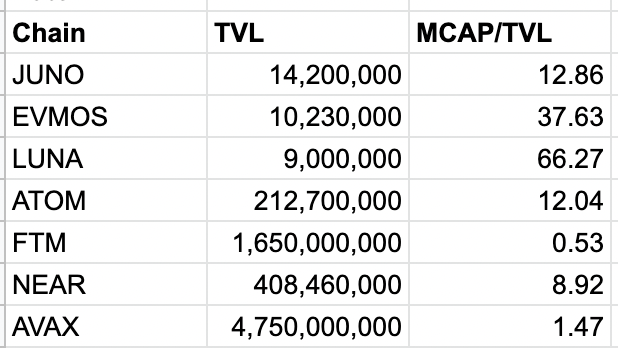

Most of the TVL is currently in Astroport at around $7.5m at the time of writing. The second AMM DEX, Phoenix, has less than $1m in TVL. There’s a total of about $9m in TVL. This makes Terra’s ecosystem one of the highest MCAP/TVL of a layer 1 at around 60 to 80 but I expect this number to slowly improve as dapps get developed and TVL flows in.

Astroport

With the Astrowars dying before it even got started, how is Astroport faring at the moment in terms of valuations?

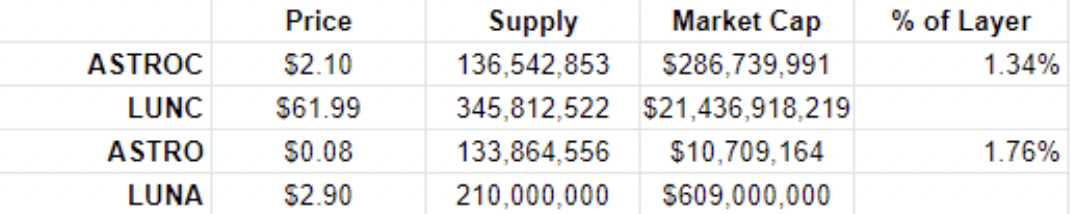

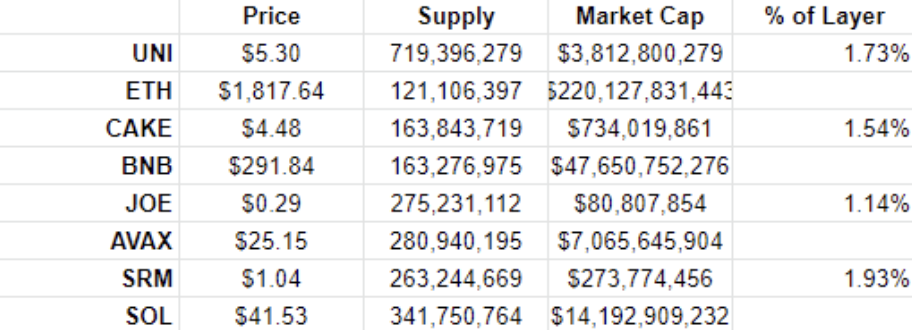

As the TVL is still slowly flowing in, we felt that it is more appropriate to just use a straight forward marketcap to % of layer comparison and we can see that Astro sits between 1-2% which is in line with other ecosystem’s main AMM DEX.

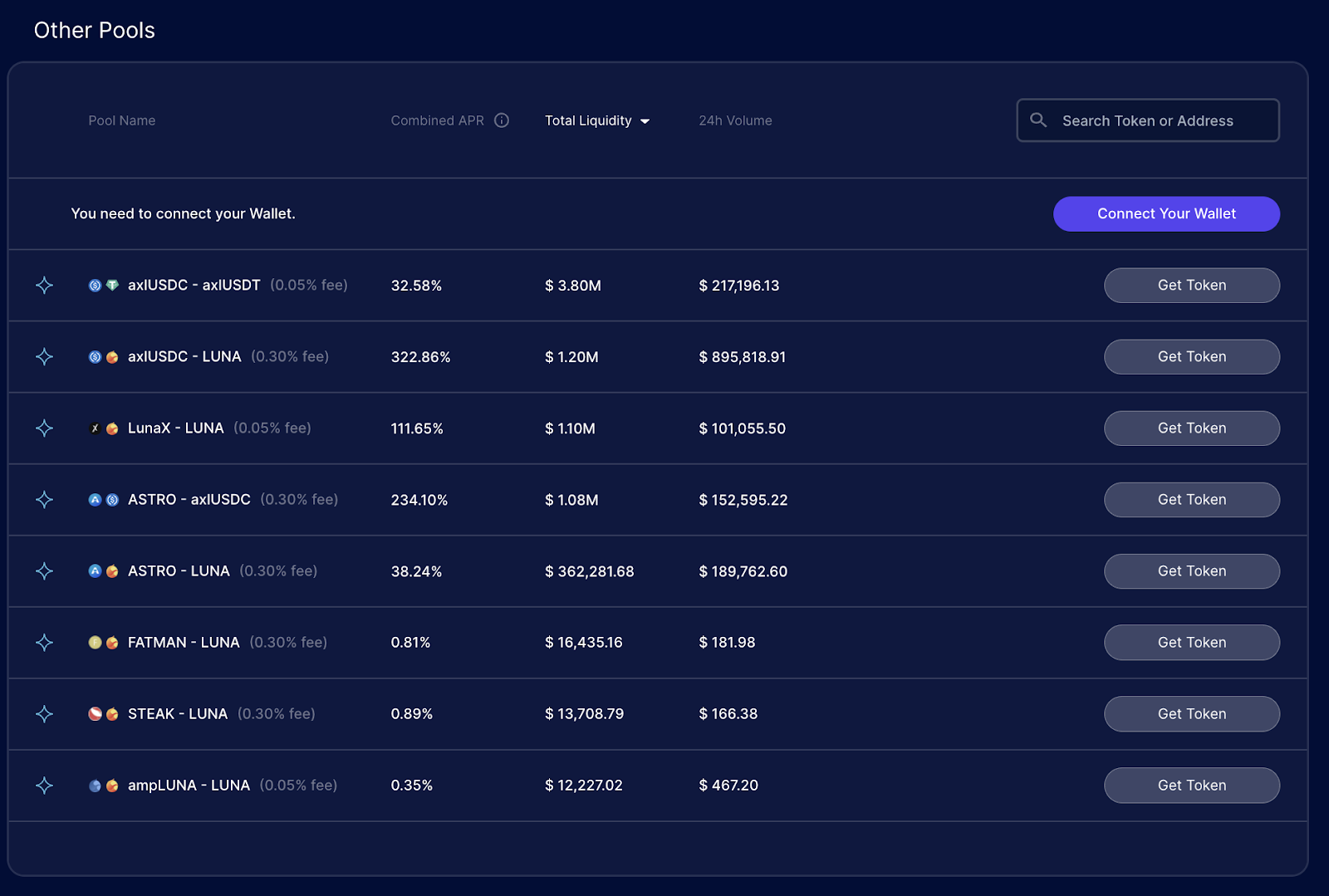

Looking at its pools, half of its TVL is in the stablecoin pair axlUSDC-axlUSDT giving about 30% APR in $ASTRO rewards. The two stablecoin comes from using satellite.money bridge powered by Axelar and carry smart contract risks as well as it is not native to Terra.

Overall, due to the tarnished reputation, insufficient venture backing, uncertainty of its future, lack of a USP, developers may be more incentivized to look elsewhere. Near, which has far more venture backing now, and also uses the same RUST programming language that Terra use, even did an open invitation to the Terra community which can be found here: https://near.org/blog/an-open-invitation-to-the-terra-community/.

It will not be surprising to see some announcements of Terra dapps launching on Near or over cosmos IBC such as Juno, or even launching their own chain entirely like what Kujira.

Web Traffic

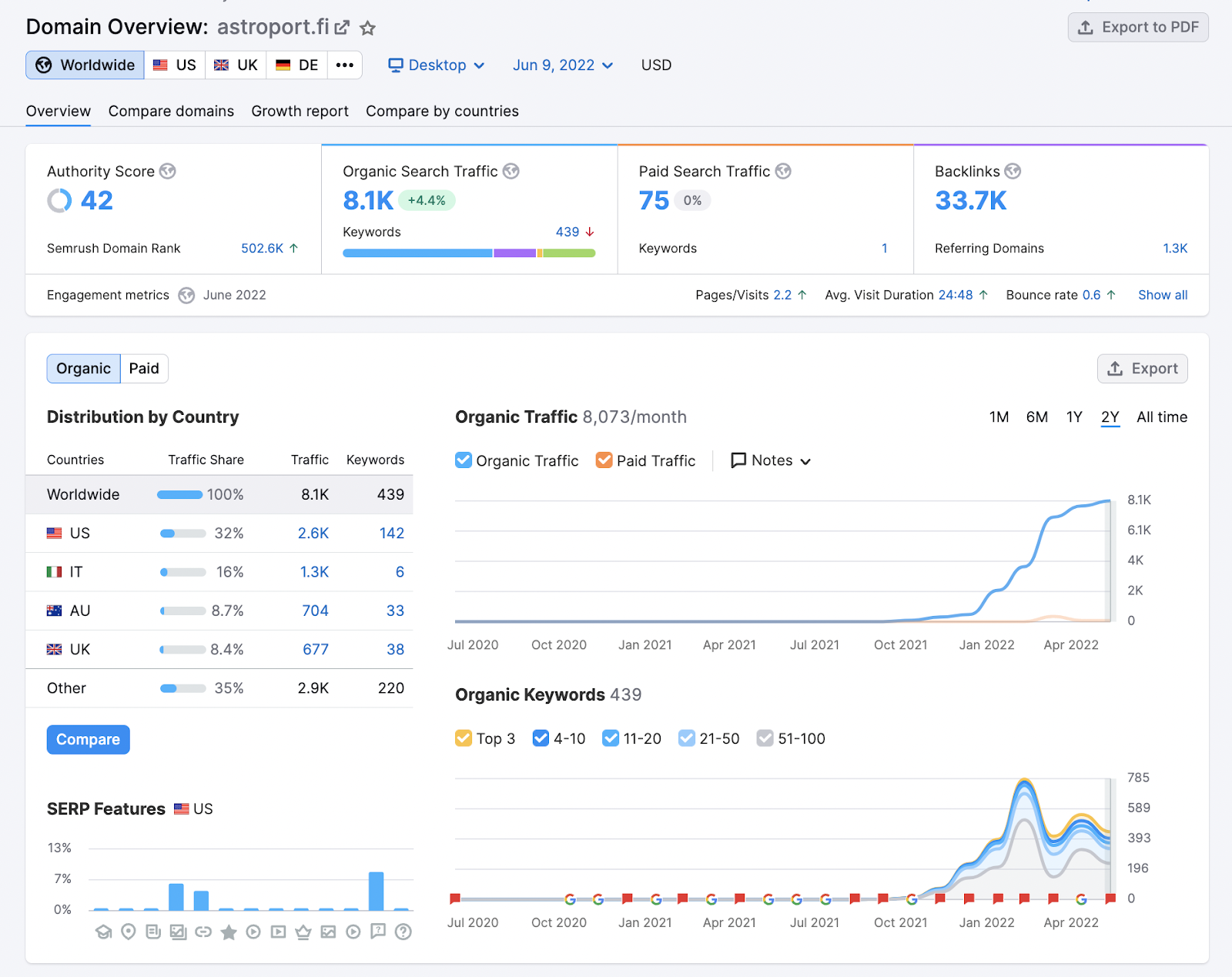

Taking a look at the web traffic of the top AMM DEXes which is where most users interact with on a network, Astroport is currently around 8,000 users per month.

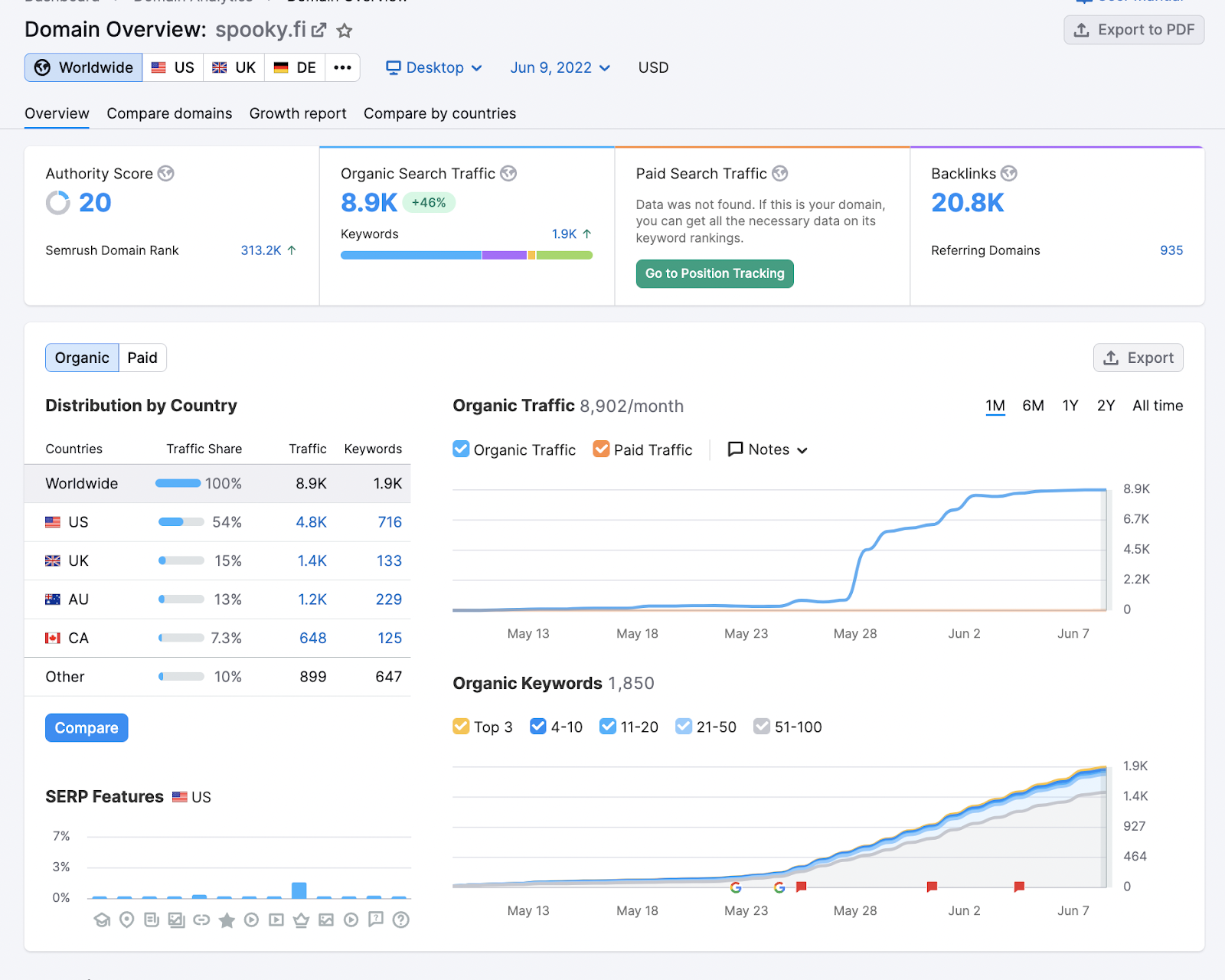

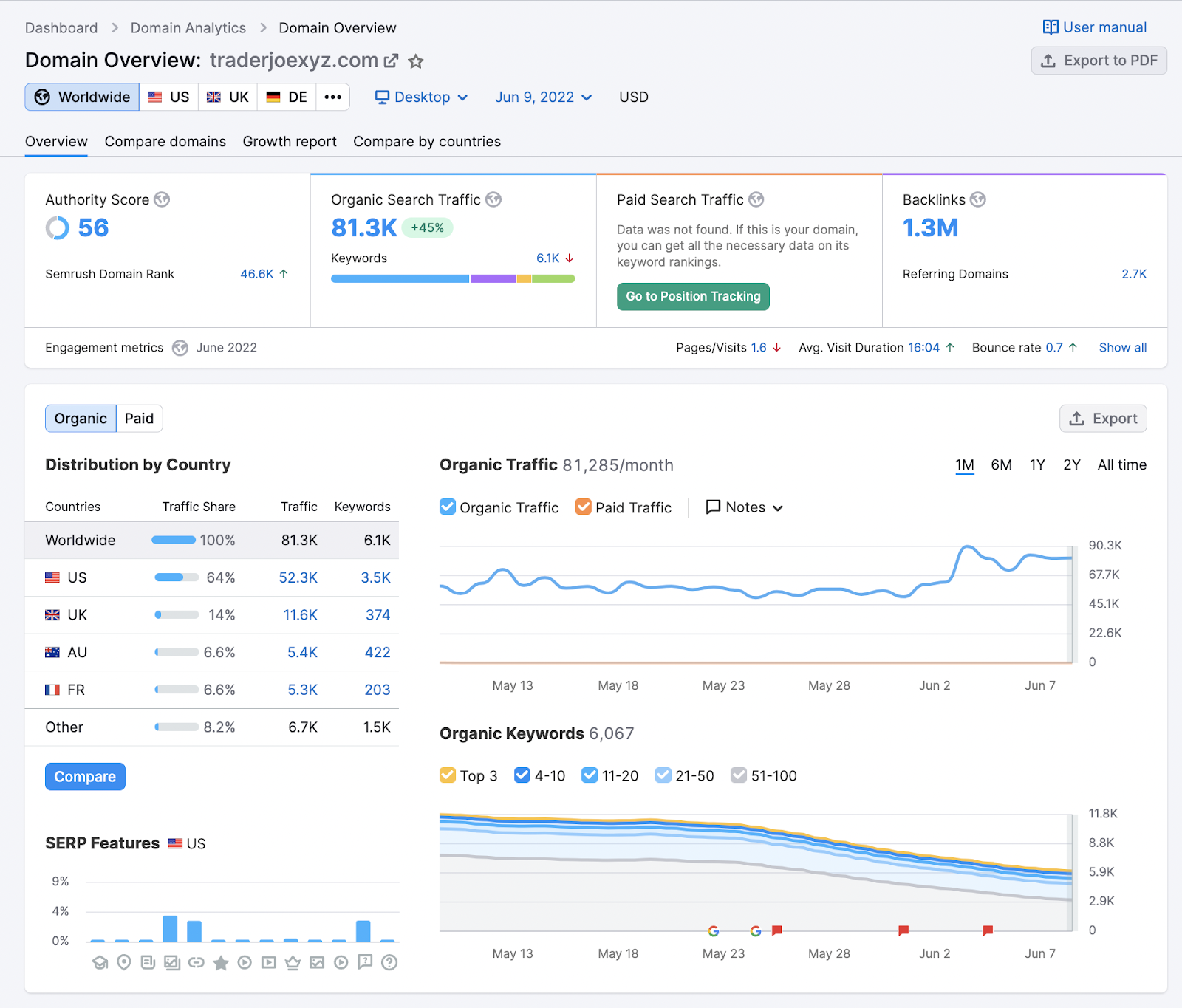

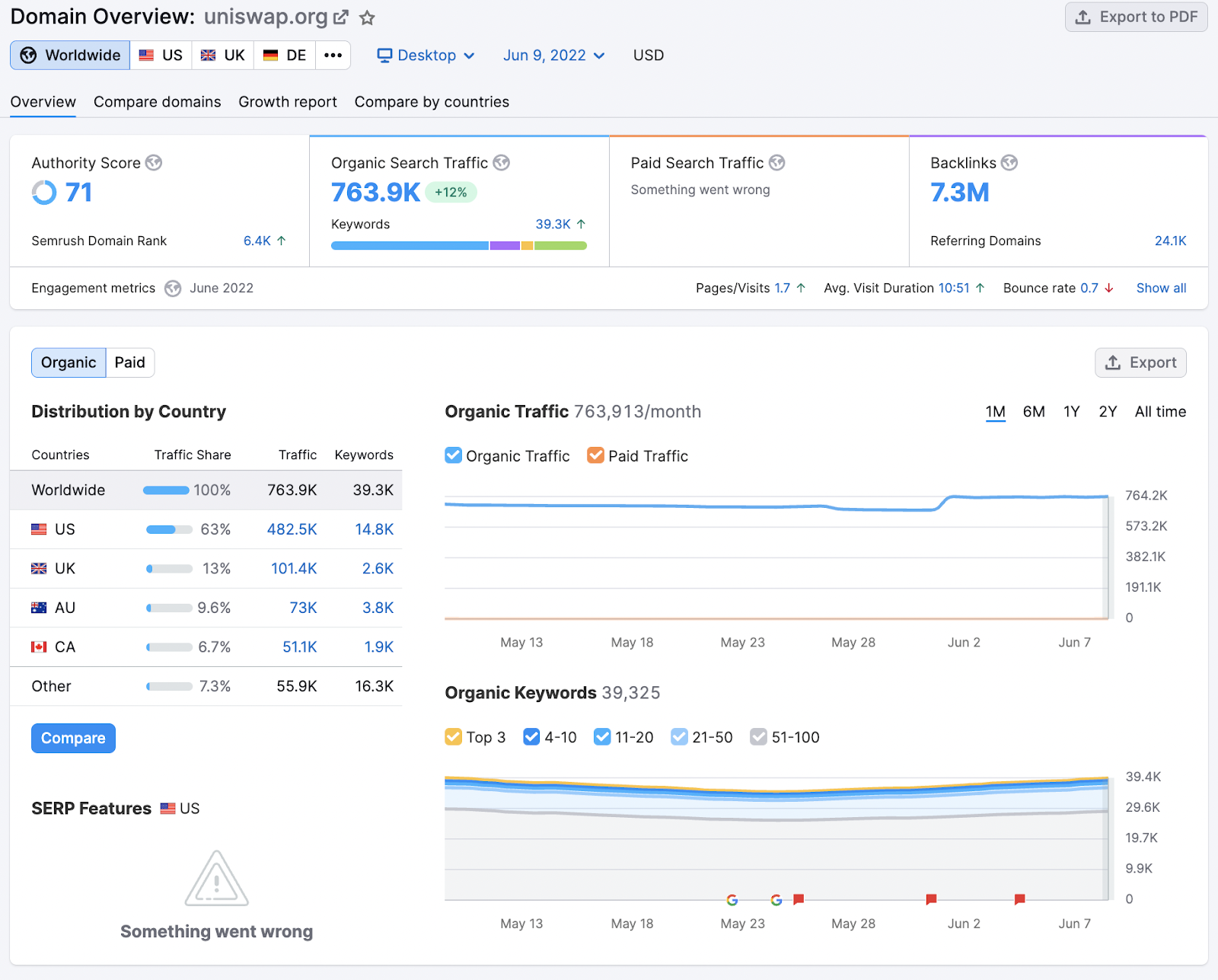

This is similar to spooky.fi, but traderjoexyz.com has 10x the traffic at around 80,000 users. None come close to Uniswap at 764,000 users per month.

No comments here for the web traffic, the numbers look reasonable for Astroport as well.

Will there be a new stablecoin?

Terra’s stable coin was its key USP and it would make sense that they would continue to find a way to create that in Terra 2.0. There are some rumors that Do Kwon might be working on a new stablecoin but those are just rumors.

Apart from Tron, which feels like a ghost chain other than USDT transfers and USDD ponzi, no other network has its own stablecoin built into the protocol level. This means that a protocol-level stablecoin will still be a USP.

However, competition is coming, such as Frax making plans to create their own roll-up chain that will probably use Frax as gas, similar to Luna 1.0. If you are wondering about Frax you can read our article here.

Although if we take a look at their CVX holdings, TFL holds the second-largest amount of CVX currently. If Terraform Labs were to do a collateralized stablecoin either in the form of MakerDAO and DAI model or a hybrid model like Frax, it will have a large advantage. It may result in LUNA regaining its USP and it is not something that should be ignored if it actually happens.

TFL’s CVX holdings: https://daocvx.com/leaderboard.

Conclusion

Based on everything we have mentioned above, Terra 2.0 feels too early, empty, and therefore speculative to invest in. Although its market cap is around $600m which is a far cry from its $40 billion market cap just a few months ago, the current tokenomics and ecosystem just do not have enough bullish catalyst to warrant investing.

If anything, if Terra approaches $5 or around $1b in market cap, it is likely a short opportunity due to its infinite supply, abysmal TVL and DApps compared to other layer 1s, and a lack of any strong buying catalyst in the foreseeable future. At $1b market cap, LUNA’s market cap will be higher than FTM, and with a much higher FDV as well(about $5b compared to $1b).

However, in the event there’s new bullish news such as a new stablecoin or more DApps returning, the situation will need to be reassessed.