Stablecoins have once again come under the spotlight, this time with AAVE introducing a new stablecoin called GHO. Let us take a look at what AAVE is and how the GHO stablecoin can improve the DeFi ecosystem.

What is AAVE?

Aave is a Decentralized Finance (DeFi) protocol that facilitates peer-to-peer lending and borrowing of cryptocurrency and dollar-valued stablecoins. Anybody can interact with these contracts without restrictions, deposit some assets in a reserve pool of funds and earn interest paid by those willing to borrow some assets from a pool.

Initially launched as ETHLend, Aave quickly rose to stardom as one of the largest DeFi lending platforms due to its ability to provide interest on a wide range of crypto deposits while issuing crypto-collateralized stablecoin loans without any credit or identity checks.

Aave is owned and governed by the Aave DAO, a global collective of token holders who vote on proposals to determine the direction and future of the protocol and thus operates like a decentralized bank run by a shareholder democracy.

Borrowing and Lending

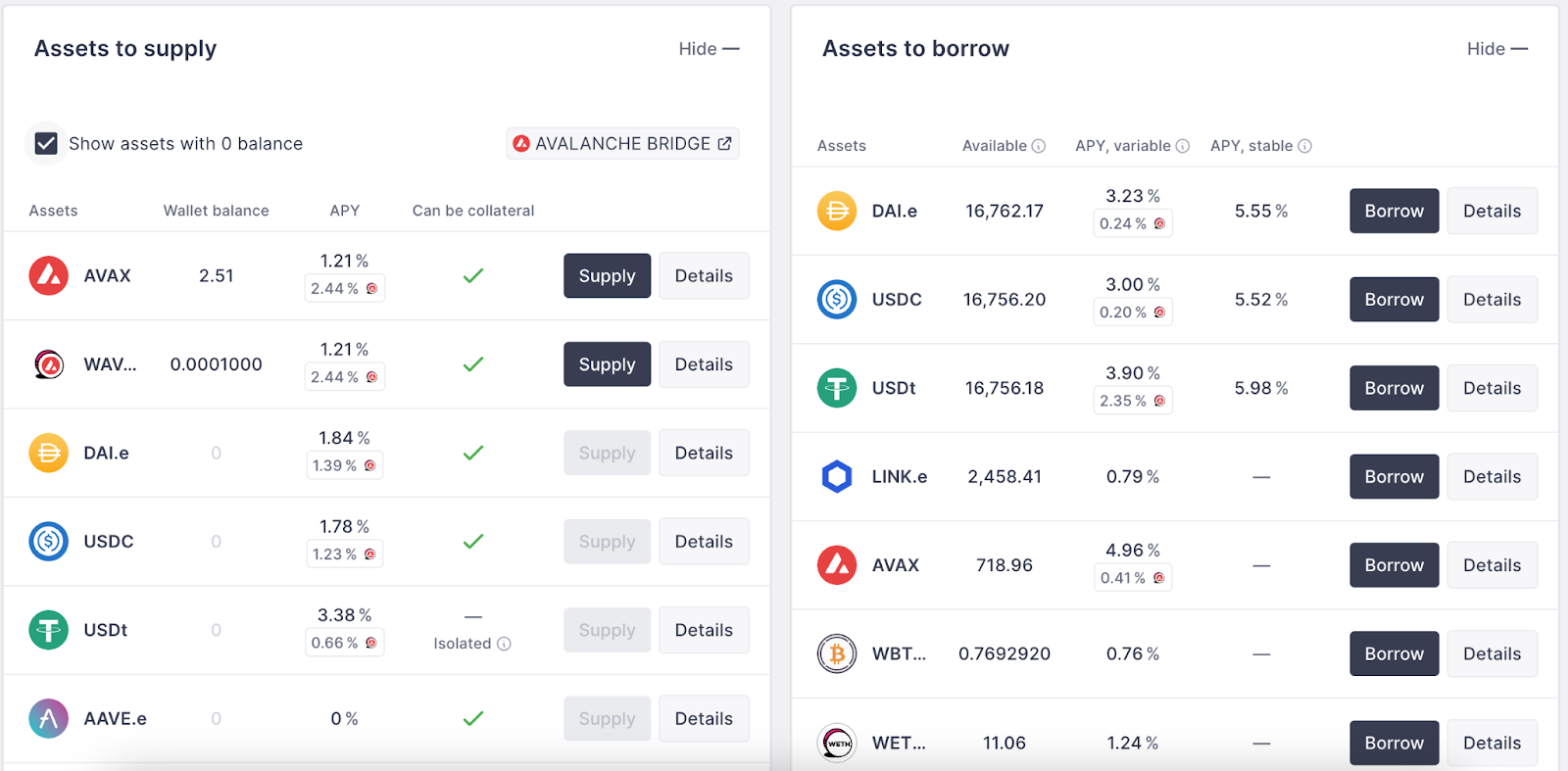

The current Aave v3 market is available on Arbitrum, Avalanche, Fantom, Harmony, Optimism and Polygon while the v2 market includes Ethereum, Polygon and Avalanche.

I will be using the Avalanche v3 market as an example.

On the left dashboard, they are the assets that can be supplied into the protocol and it includes:

- AVAX

- WAVAX

- sAVAX

- DAI

- USDC

- USDT

- AAVE

- LINK

- WBTC

- WETH

The right dashboard shows the assets that can be borrowed by users and it includes:

- DAI

- USDC

- USDT

- LINK

- AVAX

- WBTC

- WETH

To supply an asset, click on supply on the left dashboard, allow the use of your token as collateral and approve the transaction. After depositing your asset, you can now borrow another asset that is available on the protocol by going to the right dashboard and clicking on the asset which you want to borrow and approve the transaction.

Take note of the collateral ratio of each asset and your health factor after borrowing any asset as your asset supplied will be liquidated once the health factor reaches 1.00.

GHO Stablecoin

The proposal has passed and GHO will be backed by users' cryptocurrency deposits in the Aave protocol the same way DAI is backed by user deposits in the Maker Protocol.

Initially, GHO will only be available on Ethereum, but once the system has been developed, the community will vote to expand to other blockchains and Layer 2 networks, where lower gas fees may find much greater adoption.

GHO is an example of a crypto-backed stablecoin. It's a class of stablecoins that are issued as loans backed by collateralized cryptocurrency deposits and are in no way comparable to algorithmic stablecoins such as Terra's UST, which rely on clever algorithms to manage supply and demand instead of backing assets. The advantage of a decentralized design is that it does not depend on a centralized issuer (USDC and USDT) and cannot be frozen while still being fully backed by important cryptocurrencies with large market caps.

Most importantly, they do not require lenders to provide liquidity for borrowers, thus easing a major bottleneck. To date, DAI is the only memorable example of this design, but it has proven its effectiveness and stability many times over and barely twitched during UST's death spiral collapse.

Benefits to AAVE:

There are many advantages to Aave creating a crypto-backed stablecoin, especially the ability of the Aave DAO to manage the token's monetary policy. Specifically, the total supply of GHO that can be borrowed, who/what can issue GHO, and the interest rate charged for borrowing GHO.

Interest paid on GHO loans will be paid entirely to the Aave DAO. It will provide an income source of crypto and stablecoin assets that can be used to invest in the ecosystem, innovate new features, or protect the Aave treasury.

Aave V3 will also be able to issue GHO as interest payments on deposits, thus paying users in dollar-valued stablecoins instead of volatile cryptocurrencies.

The option to borrow GHO would provide greater choice to borrowers and improve stability during periods of high volatility by siphoning away borrowing demand from fatigued stablecoin pools, thus avoiding a hypothetical bank run and an ensuing liquidity crisis.

Tokenomics of AAVE

Total Supply: 16 million

- 13 million to be redeemed by LEND token holders

- 3 million allocated to AAVE ecosystem reserves

Competitors

Maker

The Maker Protocol is one of the largest dapps on the Ethereum blockchain. Designed by a disparate group of contributors, including developers within the Maker Foundation, its outside partners, and other persons and entities, it is the first decentralized finance (DeFi) application to see significant adoption.

The Maker Protocol is managed by people around the world who hold its governance token, MKR. Through a system of scientific governance involving Executive Voting and Governance Polling, MKR holders govern the Protocol and the financial risks of Dai to ensure its stability, transparency, and efficiency. One MKR token locked in a voting contract equals one vote.

The Dai stablecoin is a decentralized, unbiased, collateral-backed cryptocurrency soft-pegged to the US Dollar. Dai is held in cryptocurrency wallets or within platforms, and is supported on Ethereum and other popular blockchains.

Users generate Dai by depositing collateral assets into Maker Vaults within the Maker Protocol. This is how Dai is entered into circulation and how users gain access to liquidity. Others obtain Dai by buying it from brokers or exchanges, or simply by receiving it as a means of payment.

Once generated, bought, or received, Dai can be used in the same manner as any other cryptocurrency: it can be sent to others, used as payments for goods and services, and even held as savings through a feature of the Maker Protocol called the Dai Savings Rate (DSR).

Every Dai in circulation is directly backed by excess collateral, meaning that the value of the collateral is higher than the value of the Dai debt, and all Dai transactions are publicly viewable on the Ethereum blockchain.

One problem with Dai is that, although they are a decentralized stablecoin, more than half of its collateral is made up of USDC as shown here. This poses centralization risks and might defeat the purpose of having a decentralized stablecoin that is majority backed by a centralized stablecoin.

Compound

Compound is a protocol on the Ethereum blockchain that establishes money markets, which are pools of assets with algorithmically derived interest rates, based on the supply and demand for the asset. Suppliers of an asset interact directly with the protocol, earning a floating interest rate, without having to negotiate terms such as maturity, interest rate, or collateral with a peer or counterparty.

Unlike an exchange or peer-to-peer platform, where a user’s assets are matched and lent to another user, the Compound protocol aggregates the supply of each user; when a user supplies an asset, it becomes a fungible resource. This approach offers significantly more liquidity than direct lending; unless every asset in a market is borrowed (see below: the protocol incentivizes liquidity), users can withdraw their assets at any time, without waiting for a specific loan to mature.

Compound also allows users to frictionlessly borrow from the protocol, using cTokens as collateral, for use anywhere in the Ethereum ecosystem. Unlike peer-to-peer protocols, borrowing from Compound simply requires a user to specify a desired asset; there are no terms to negotiate, maturity dates, or funding periods; borrowing is instant and predictable. Similar to supplying an asset, each money market has a floating interest rate, set by market forces, which determines the borrowing cost for each asset.

Frax Finance

Frax is the first fractional-algorithmic stablecoin protocol. Frax is open-source, permissionless, and entirely on-chain – currently implemented on Ethereum and 12 other chains. The end goal of the Frax protocol is to provide a highly scalable, decentralized, algorithmic money in place of fixed-supply digital assets like BTC.

The Frax protocol is made up of 2 tokens, the FRAX stablecoin and FXS governance token. FRAX can be minted with a % of collateral in USDC and FXS. At the point of writing, 88.75 cents worth of FRAX and 11.25 cents worth of FXS is needed to mint $1 of FRAX and vice versa for redeeming FRAX. As the peg becomes more trusted, the collateral ratio will drop, resulting in more FXS needed to mint FRAX.

Curve Finance

Curve Finance are also likely to be creating their own stablecoin called crvUSD. According to an interview with the Curve founder, crvUSD will be an over-collateralized stablecoin, similar to DAI. However, there is not much information about how their stablecoin is going to be minted at the moment.

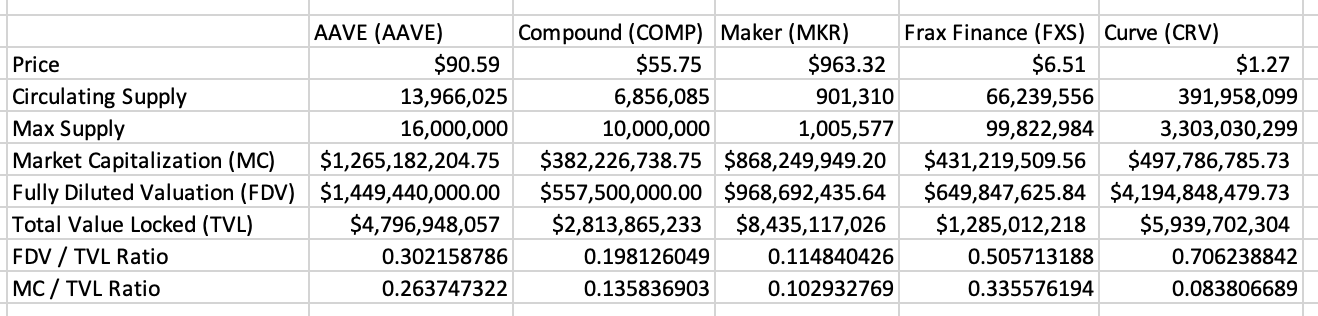

Valuation Comparison

Conclusion

Despite only being around for about 2 years, AAVE has already established themselves as one of the blue-chip protocols in the cryptocurrency space. The Aave team are also currently working on a decentralized social media platform called Lens Protocol. With the launch of GHO, they will be trying to gain a spot in the stablecoin ecosystem, which could bring them further ahead of their competitors.

Currently, stablecoins amount to a massive $154 billion market capitalization. This is due to their usefulness in hedging against cryptocurrency volatility and serving as a global payment method, but they have found their best use cases in DeFi lending/borrowing dApps.

However, the largest crypto-backed dollar stablecoins (USDT, USDC, BUSD) are run by centralized companies backed by cash reserves. Therefore, launching a DAI competitor with Aave's lending/borrowing system makes sense, both in terms of innovation and business strategy.

Furthermore, Maker Protocol is often regarded as the "central bank of DeFi," as its DAI token is currently the top decentralized stablecoin but is backed majority by a centralized stablecoin. This makes Aave in a good position to potentially take its place as the DeFi King with GHO, further increasing their revenue and market share in the ecosystem.