Content:

- The Liquidity War Begins

- Curve Wars, Bribes, and Cartels

- What is Astroport?

- What is $ASTRO?

- The Astro Wars

- Bribing Flywheel

- Tokenomics

- Conclusion

The Liquidity War Begins

Let’s talk about liquidity.

One of the key things in decentralized finance (DeFi) is liquidity and incentives. Locking up tokens into a liquidity pool means users can’t sell the tokens, and selling tokens into a deep liquidity pool doesn’t move the price much, and the price can remain high.

In order to get market participants to lock up their tokens, clever incentives are designed to motivate that behavior. On the other hand, tokens with poor incentives usually see tokens going to zero in value.

For DeFi to succeed, we need to design incentives to keep tokens locked up, and the two biggest participants in DeFi are liquidity attractors and liquidity providers.

Liquidity attractors want to spend as little as possible to attract and preserve as much liquidity as possible. Liquidity attractors need liquidity for their operations, these include decentralized and centralized exchanges as well as individual protocols who benefit from having liquidity in exchanges.

Liquidity providers on the other hand seek to gain the highest yield on their assets with as little risk as possible.

In a study by Lioba Heimbach, Ye Wang and Roger Wattenhofer, behaviors of liquidity providers were analyzed to find out that users of cryptocurrency ecosystems have gradually become interested in providing liquidity in DEXes.

However, users were still cautious – preferring to participate in few liquidity pools. The returns and losses of providing liquidity in different types of pools vary a lot. Stable pools enable a near risk-free and profitable investment opportunity. Providing liquidity in volatile pools, on the other hand, appears to perform much worse than the corresponding constant-mix portfolios.

Source:https://arxiv.org/abs/2105.13822

To understand more about liquidity wars, let us first explain Curve - the top stableswap exchange.

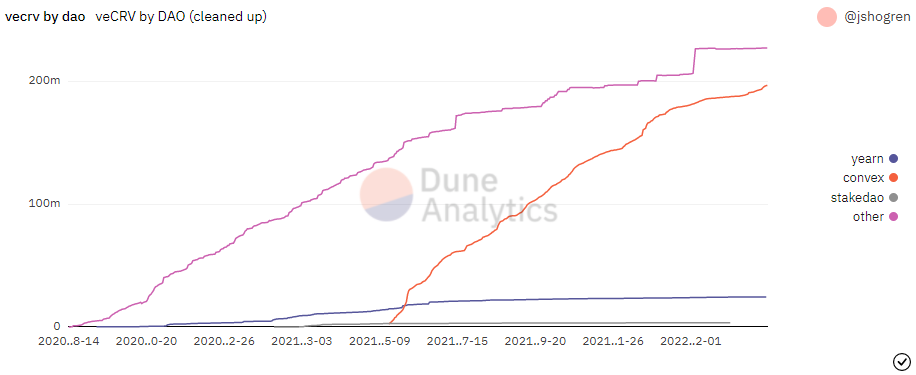

Curve Wars, Bribes, and Cartels.

Curve has created a low slippage trading environment for stable assets while providing the ability for liquidity providers to earn attractive yields, due to its deep liquidity pools and proprietary formula.

This incentivizes a large amount of trading volume, especially from whales, which in turn rewards liquidity providers through trading fees and $CRV tokens.

As liquidity providers are also paid in $CRV, this increases the total reward for certain pools. While most reward tokens are inflationary with no use case aside from governance, $CRV provides additional utility in the form of boosts to counter token inflation.

$CRV tokens can be locked for up to 4 years to boost your farms. Furthermore, governance is extremely important as you can vote for which liquidity pools get additional incentives in the form of $CRV.

The Curve War has led to increased buying pressure for $CRV as the race between various protocols continuously try to ensure that their preferred pools offer the highest $CRV rewards.

Since bribing with their native tokens for prolonged periods could lead to massive selling pressure, many protocols such as Abracadabra, Yearn Finance, Stake DAO, and more, are accumulating $CRV to boost emissions for their own project’s liquidity pool. This has proven to be more cost saving than giving their native token as liquidity reward.

On top of that, aggregator protocols building on this concept of $CRV boosts have also been created, such as Convex Finance ($CVX) and Redacted Cartel ($BTRFLY). They would either directly or indirectly aggregate and lock up $CRV tokens for $veCRV (vested & locked $CRV).

Protocols looking to attract liquidity will pay $CVX holders to vote because it is far more cost effective to ‘bribe’ them to vote on your protocol to boost emissions than to acquire $CVX on their own to vote for their own protocol.

We have gone through one of the most complex protocols in DeFi, and this is all related to Astroport so let’s do a quick recap:

- Protocols that can attract and lock up deep liquidity in a dex will have better price action

- Aggregators are created to consolidate voting power by accumulating the dex token

- Voting power can be used to sway votes to incentivize chosen pools to attract liquidity

- Protocols buying aggregator tokens to sway votes to incentivize liquidity perform better

- Protocols providing liquidity reward via their own native tokens have high sell pressure

All of these can be translated to Astroport, where we will be taking a look at $ASTRO, $xASTRO and $vxASTRO, as well as $ASTRO aggregators.

What is Astroport?

Astroport is the biggest decentralized exchange (DEX) on Terra, with over $800 million in TVL on the protocol. As of writing this, Astroport has a 24 hour volume of $200 million, netting the protocol over $450K in trading fees daily. With more users coming onboard to use Astroport, it’s only a matter of time before we see the protocol catching up to similar revenue generated from other large DEXes.

What makes Astroport unique is that they have both stableswaps and constant product swaps.

What is $ASTRO?

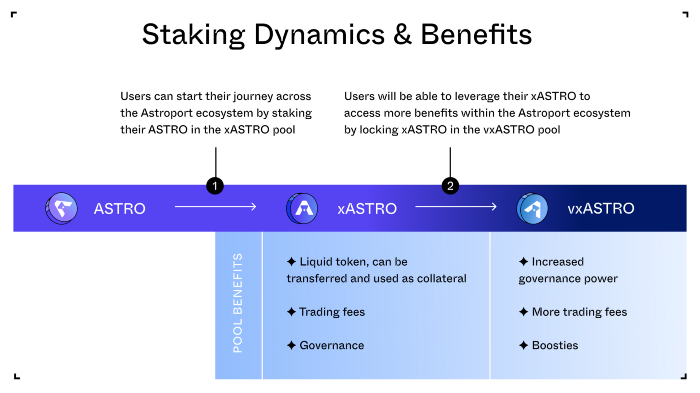

$ASTRO is the governance token of Astroport that allows stakers to receive $xASTRO while earning fees generated by the protocol in the form of additional $xASTRO. $xASTRO holders can also lock their tokens to receive $vxASTRO

$vxASTRO is not a transferable token but can be seen as a points system similar to veCRV that gives you additional benefits based on how long your tokens are locked, such as earning extra trading fees and having increased governance power.

These fees are distributed to liquidity providers and $xASTRO holders. Liquidity providers are rewarded in the form of LP tokens and additional incentives, while stakers are rewarded in $ASTRO that are bought from the open market.

With the recent release of $xASTRO and upcoming launch of $vxASTRO, Astroport has been buying back tons of $ASTRO to reward stakers, causing the price of $ASTRO to spike.

An example for locking 100 $xASTRO (up to 2 years) would give you,

- 2 years $xASTRO lock = 200 $vxASTRO

- 1 year $xASTRO lock = 100 $vxASTRO

- 1 month $xASTRO lock = 8.3 $vxASTRO

Since staking and locking $ASTRO is required to govern the protocol, those with the most $ASTRO will have control over which pools on Astroport get to receive the most rewards as incentivized pools will be able to receive up to 250% of regular $ASTRO emissions.

However, most people are not keen to lock up their tokens for 2 years due to the fast paced environment in DeFi. Similar to Curve, other protocols can then either buy up $ASTRO or bribe users to vote for their pools with their native tokens.

The Astro Wars

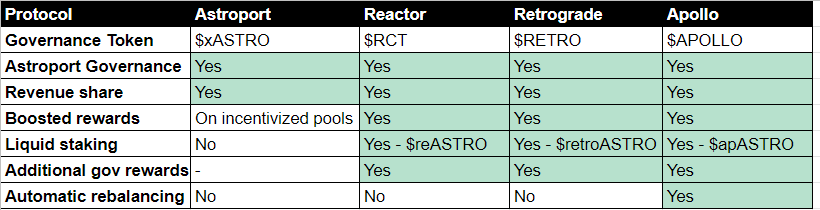

This is where the war begins. There are 3 main protocols fighting in this war. They include Reactor, Retrograde, and Apollo. This will benefit holders of $ASTRO as these protocols will fight to buy up $ASTRO tokens, increasing its value.

These protocols will buy and stake $ASTRO, locking up $vxASTRO permanently in their treasury, This will redirect a portion of boosted yield from Astroport to their native token stakers.

Using Reactor as an example. When a user locks $ASTRO on Reactor, they receive a liquid derivative token ($reASTRO) that corresponds one to one with the $ASTRO in their treasury.

Unlike $vxASTRO which is illiquid and has limited utility, $reASTRO tokens can be further staked on Reactor to earn $RCT on top of $vxASTRO rewards, which includes Astroport trading fees and boosted rewards. They can also be swapped into $ASTRO at any time which makes it very attractive to most people.

Since Reactor distributes a portion of rewards from Astroport to their stakers, this means that users can earn $ASTRO rewards through their protocol without having to provide liquidity on Astroport or hold any $ASTRO tokens.

While users enjoy the benefits of these protocols, they are accumulating more $xASTRO to increase their governance power. This is to ensure that users incentivize their own pools through these bribing protocols so that they can earn even more rewards for providing liquidity.

Additionally, other protocols or new protocols who are looking to increase the liquidity of their pools can bribe $vlRCT holders (staked $RCT) to direct liquidity to their pools, part of these bribes will be given to $reASTRO holders.

Bribing Flywheel

Let’s take a deeper look at the bribing protocols of Astroport, specifically Reactor.

As Reactor accumulates $ASTRO, it incentivizes liquidity providers to provide $ASTRO to lock up more $xASTRO and thus earning more points which earns more $ASTRO boosted rewards and $RCT. This increases the revenue of the protocol which increases the value of $RCT. This attracts more $ASTRO liquidity to Reactor, creating a positive flywheel effect for $RCT.

Apollo has a unique liquid staking mechanism which is unlike Reactor and Retrograde. When depositing $ASTRO to Apollo, it becomes $apASTRO which is a yield bearing $ASTRO asset and grows in value overtime. On the backend, 50% of the $ASTRO is converted into $zvxASTRO at a 1:1 ratio.

$zvxASTRO is $vxASTRO but it also earns Astroport swap fees as well as $APOLLO incentives. $zvxASTRO is then paired together with the other 50% of your $ASTRO to form the $zvxASTRO-$xASTRO liquidity pool, which is then deposited into a vault that auto compounds the fees and the $APOLLO incentives. The value of this pool is reflected in the increase in value of your $apASTRO.

Here is a summary of Astroport’s bribing protocols.

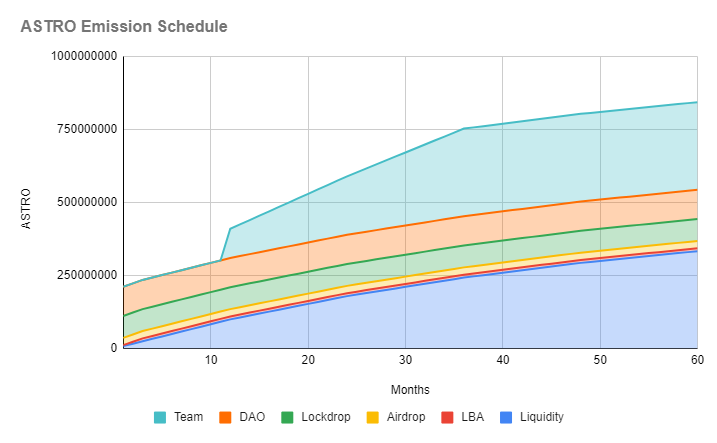

ASTRO Tokenomics

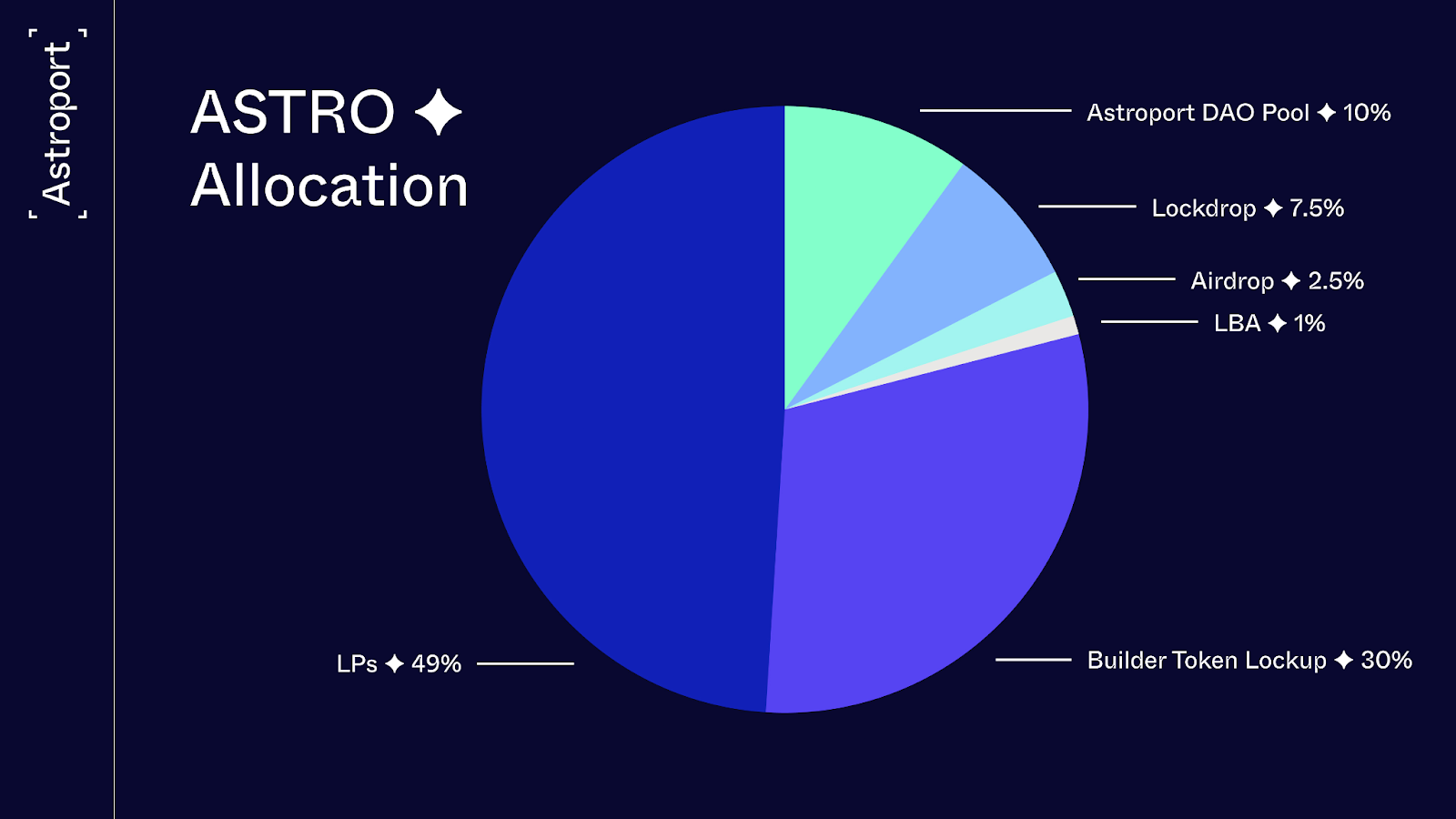

There will be a maximum supply of 1 billion $ASTRO.

Token Distribution:

Team: 30% (10% unlocked after 1y, 20% vested over 2y)

LBA: 1%

Airdrop: 2.5%

Lockdrop: 7.5%

DAO Pool : 10%

LP Emissions (69 years): 49%

84% of all emissions released within the first 5 years, while the remaining $ASTRO is released across 69 years.

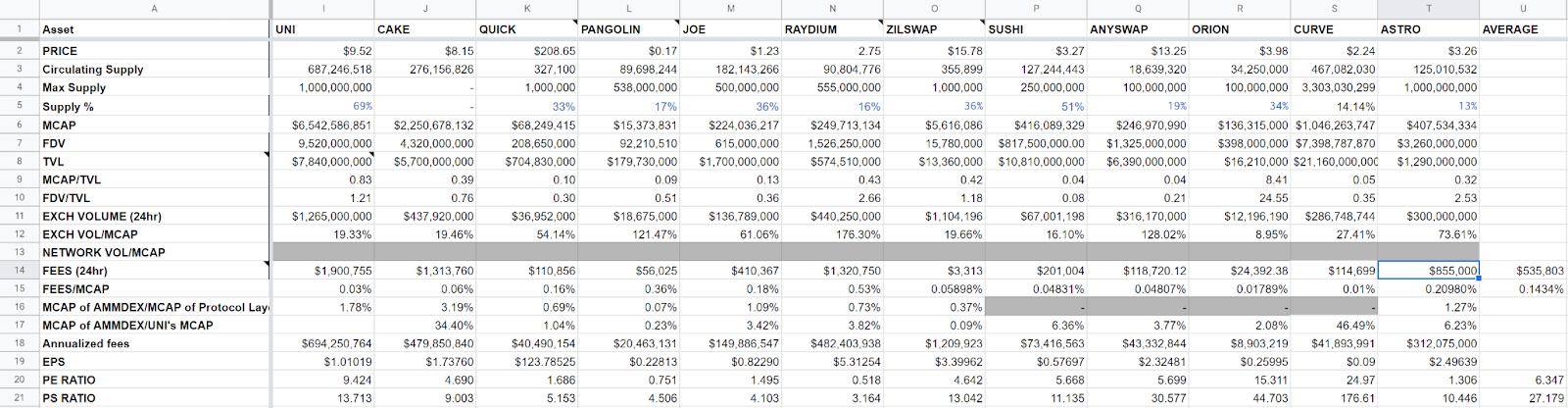

Valuations

Astroport generates around $855K in daily trading fees based on the average 24 hour trading volume of $380 million, 0.3% from constant product pools and 0.05% from stable pools.

Astroport’s Financials:

MCAP/TVL = 0.34

FDV/TVL = 2.74

P/E = 1.30

P/S = 10.44

Average AMM Dex’s Financials:

MCAP/TVL = 0.93

FDV/TVL = 2.86

P/E = 6.326

P/S = 27.122

Compared to the average P/E and P/S ratio of other DEXes, Astroport seems undervalued even at the price of $3.25.

Conclusion

As other protocols join the fight for $ASTRO to direct liquidity to their own pools, this would drive the price of $ASTRO up. This benefits smaller participants too as they will be able to earn the rewards without locking up their $ASTRO for a long time.

We started researching and writing this article when $ASTRO was less than $1 when we felt it was severely undervalued, and even above $3 we remain bullish on the future of $ASTRO as it has strong financial numbers backing its valuations.

However, DeFi is a rapidly changing space and if trading volume on Terra dries up during a bear market, we could see $ASTRO price adjusting back down as well. It will be exciting to see how the bribing war plays out once Astroport bribing goes live.

Huge thanks to @farmertuhao, @packformoon and @apedigest for their twitter threads.